Manufacturing Accounting: Everything You Need to Know

As part of the manufacturing process, your business is likely to have items in production that have not yet been completed. Technology and global trends are always changing – and so must a manufacturing business if it wishes to stay agile. By the time you finish upgrading your systems, the world may have evolved to make them obsolete.

Therefore, it’s important to have specific accounts dedicated to tracking the inventory of raw materials. These accounts allow you to monitor the quantity and value of raw materials on hand, ensuring accurate costing and inventory management. Another important aspect to consider when creating your chart of accounts is to incorporate cost centers. Cost centers are specific departments or areas within your manufacturing business that incur costs. By assigning each cost center its own set of accounts, you can track expenses and allocate costs more accurately.

Cost of Goods Sold Manufacturing Account

It’s wise for a manufacturing accountant to follow shifting customer trends as a change in demand could drastically alter the cost landscape for the business. These include things like rent, asset depreciation, marketing, and office expenses – all of which may be necessary to operate a manufacturing business. In the following article, we will discuss how accounting for manufacturing differs from mainstream applications and share best practices for success. If you’d like to learn more about chart of accounts and explore other related topics, feel free to check out our chart of accounts guide for a deeper dive into this essential financial tool.

- You have now reached the end of our comprehensive guide on mastering the chart of accounts for manufacturing businesses.

- This will be an accumulation of the money you have spent on direct materials, direct labor costs, and manufacturing overheads on each work-in-process item in your inventory.

- Direct materials refer to the raw materials that manufacturers transform into finished products.

- So, let’s embark on this journey to master the chart of accounts for manufacturing and unlock the full potential of your business’s financial management.

An automated inventory management system facilitates accurate inventory accounting and can greatly reduce the time and cost required to manage physical stock. There are likely hundreds of software tools available that help with accounting for manufacturing costs. You’ll need to speak with your accountant or financial advisor and consider your current budget before making an informed decision. Accounting for manufacturing overhead costs requires more effort, and can be more challenging compared to other costing efforts because of the difficulty in assigning them to specific products or outcomes. Manufacturing overhead costs are indirect costs that are incurred during a particular accounting period but cannot easily be accounted for on a per-unit basis.

What is Manufacturing Accounting?

Typically, manufacturers handle a variety of materials, goods, and final products that you must carefully monitor. Once the manufacturing process is complete, products become finished goods ready for sale. Having separate accounts for finished goods inventory enables you to monitor the value of the goods available for sale, ensuring accurate financial reporting and inventory control.

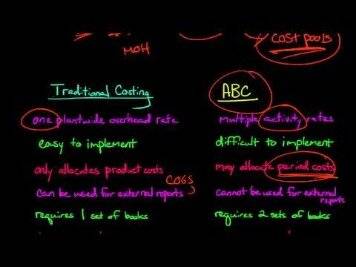

The process also grows progressively more complex as your operation grows in size and may call for better and more efficient costing and accounting methods to ensure you’re running a sustainable business. Activity-based costing (ABC) accounts for the overhead and indirect costs used to manufacture a product. If the toothpick shaper employee makes $50 per hour and can shape 1,000 toothpicks per 10 business development tips for attorneys hour, then the activity-based cost of the shaping operation is $0.05 per toothpick. Adding up the ABC of all operations provides the total ABC for a finished good. Activity-based costing (ABC) is a way to assign indirect manufacturing costs like overhead to products or processes. Though it takes more work than applying a standard overhead rate, it generates more accurate cost estimates.

What type of accounting is used in manufacturing?

In simple terms, it is a comprehensive list of all the different types of accounts that your business uses to record financial transactions. Each account represents a specific category or classification, such as assets, liabilities, revenue, or expenses. The direct labor Manufacturing account tracks all of the wages paid to workers directly involved in the production process. Direct labor is the value given to the workers who manufacture your products. Direct labor costs typically include wages paid for regular hours, overtime and payroll tax information. This strategy can be used when the production process is completed over many different stages.

In standard costing, businesses assign standard costs for raw materials and labor when factoring them into inventory and production expenses. Standard costing enables manufacturers to follow through with the production process based on a set standard which can later be reassessed based on the variance they calculate by zeroing in on each stage of production. In manufacturing accounting, various financial aspects are addressed, including the cost of raw materials, labor, overhead expenses, and inventory valuation. The primary objective is to provide insights into the financial performance and profitability of manufacturing activities, enabling informed decision-making and effective cost management. Job costing often involves the cumulation of costs involved in procuring materials, labor expenses, and manufacturing overheads. The job costing process is perfect for businesses that custom-make products for their clients.

What is the approximate value of your cash savings and other investments?

These details enable the production managers to attune production practices to ensure the business remains efficient in production and saves costs while maximizing returns from sales. Unlike retail and service-oriented operations, manufacturing businesses face a special set of challenges regarding accounting and costing methods. Manufacturing businesses need to maintain a close watch on their books to ensure they generate the required amount of profit relative to their costs since they create products from scratch. Both offer greater tax-planning flexibility, allowing some businesses to defer taxable income.